Why does capital flow from equal to unequal countries? This question is at the heart of my research with Sergio de Ferra and Kurt Mitman.

First, we document a new empirical fact: among advanced economies, unequal countries like the UK and the USA tend to accumulate fewer assets in the rest of the world than more equal countries do, such as those in Scandinavia. Second, we present a theory for why this happens: more unequal countries develop deeper financial markets. Therefore, households living in unequal countries can borrow more than households in equal countries. Well, that is the research in simple terms, but let’s look at it in more detail.

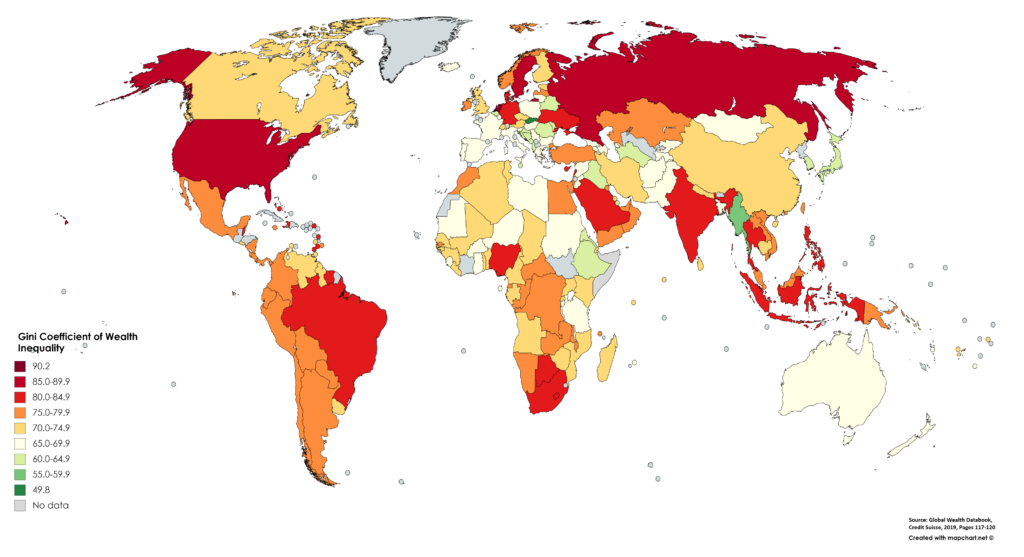

In our study, we measure income inequality across countries using the Gini index for income after taxation. The Gini index is a measure of statistical dispersion widely used to measure income and wealth inequality; a higher Gini means higher inequality. We combine this data with the main measure of a country’s external saving or borrowing, the current account balance to GDP ratio. The current account balance represents how many external assets a country accumulates or decumulates in each year. A country with a positive current account lends to foreign residents, while a country with a negative current account borrows from foreign residents. Economists generally think that, on average, a country’s current account should equal zero, especially among advanced economies. However, important countries in this group, such as the United Kingdom or the United States, have consistently run current account deficits in recent decades. Understanding the causes of these deficits is an important open question in international macroeconomics, and our research contributes to answering it.

Our paper is the first to document that the correlation between the current account balance and income inequality is negative. Countries with high income inequality tend to run current account deficits, while countries with low income inequality run current account surpluses. Further, we show that this negative correlation arises from a negative correlation between private savings and income inequality. In countries with high income inequality, the private sector saves less than in countries with low income inequality.

Our empirical result is surprising since the standard models in macroeconomics would predict the opposite. To understand why we must first explain the two main causes of income inequality, known as persistent and transitory income risk. First, individuals might differ in terms of persistent characteristics that empirically are associated with different income trajectories, such as education or skill. A more highly educated person tends to earn more than a less educated one. The typical heart surgeon earns a much high income than a bus driver, for example. However, as these differences tend to persist throughout these individuals’ lives, individuals with higher income would have higher levels of consumption and not necessarily of savings. In concrete terms, the heart surgeon can enjoy fancier holidays and a larger car than the bus driver. If differences in income inequality across countries were mainly due to differences in persistent income risk, we would thus expect a similar level of external saving between equal and unequal countries.

A second reason for income inequality is that the same surgeon or bus driver can lose their job and thus experience a period of their life where their income is temporarily lower. Economists call this transitory income risk. The higher this transitory income risk, for instance because of a high probability of losing a job or because of a big drop in earnings when this happens, the higher this income inequality. However, here comes the twist: a person who lives in a country with a high income risk should save more, according to traditional macroeconomic models. This is because having a stock of savings would allow this person to sustain higher consumption in periods of low income – an economic force known as the precautionary saving motive. Therefore, if transitory income risk is the main driver of income inequality, we would expect individuals in countries with high inequality to save more and the country as a whole to run a larger current account surplus. Puzzlingly, we document the exact opposite. Hence, we had to develop a novel theory to explain this novel fact.

We consider a model economy where households can default on their debt. If they default, they are not allowed to borrow in financial markets for several periods. Thus, their consumption cannot be higher than their income, and they cannot run up debt to deal with periods of temporarily low earnings. An individual living in a country with low income risk does not attach a high value to participation in financial markets. For this individual, the punishment of being excluded from the financial markets is small, since there is not a big risk of earnings falling much. Therefore, this individual has a strong incentive to default on their debt, even when such debt is small. Hence, going back one step, they will not be able to borrow much from financial markets. The opposite is true for households living in countries with high income risk. They value participation in financial markets highly. Therefore, they will repay even high levels of debt, and they will be able to borrow substantial amounts of resources. In countries with high income risk, deeper financial markets thus emerge, providing greater insurance to households who value participation in such markets highly. Thus, households in countries with high income risk can borrow more than households in countries with low income risk. Therefore, exactly as we find in the data, more unequal countries save less than less unequal countries.

We find this research avenue very exciting, as it touches upon themes of inequality and financial globalization, which both myself and my co-authors see as some of the most critical issues of our time. While our research so far has focused on advanced economies, we will soon begin to explore similar forces among emerging market economies, where much of the recent economic growth has taken place. We plan to work for many years ahead on this and related topics, and we hope to gain many more important insights for researchers and policy-makers.